All amounts are in United States dollars, unless otherwise stated.

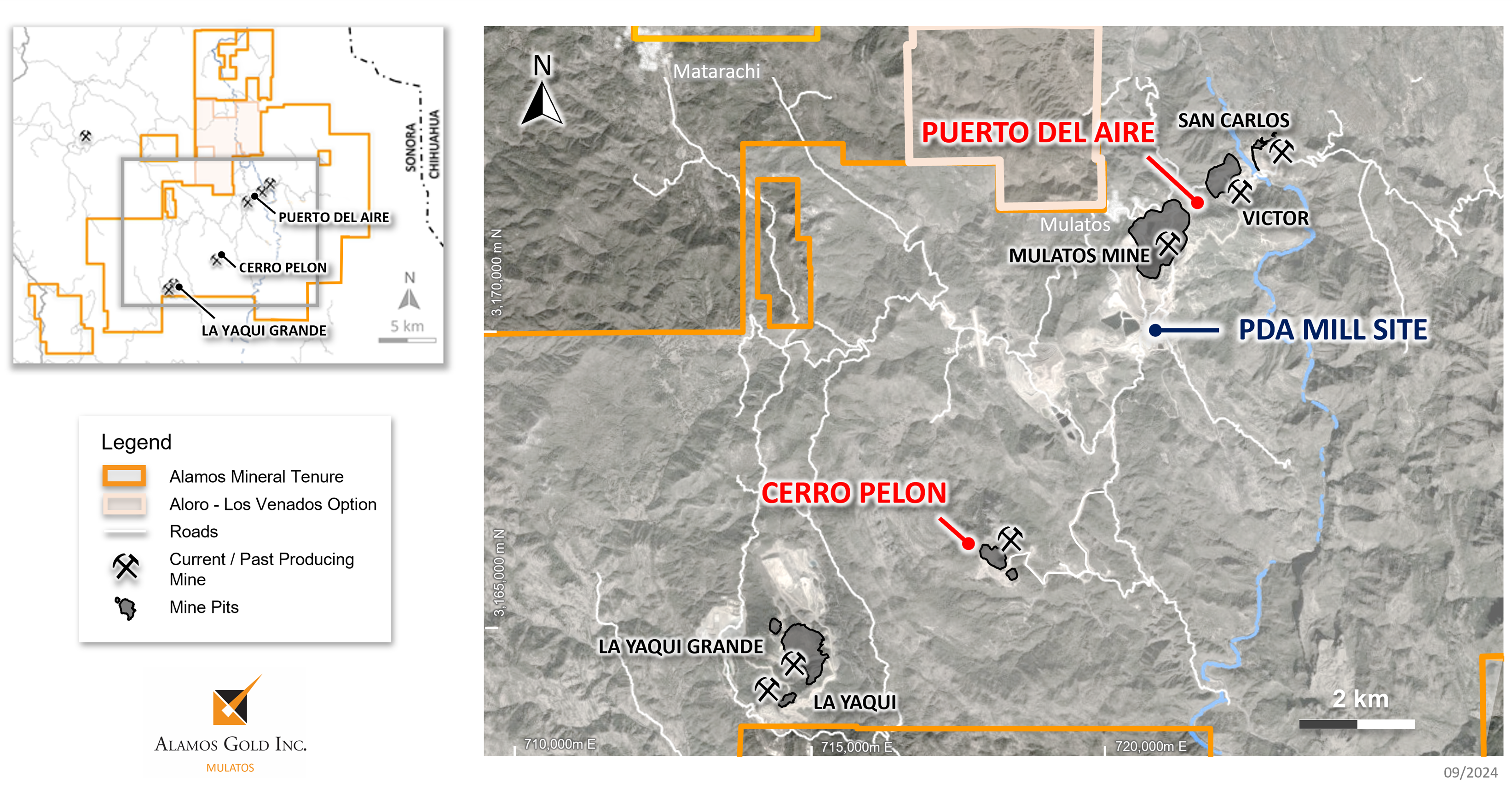

TORONTO, Sept. 04, 2024 (GLOBE NEWSWIRE) -- Alamos Gold Inc. (TSX:AGI; NYSE:AGI) (“Alamos” or the “Company”) today reported results of the positive internal economic study completed on its Puerto Del Aire (“PDA”) project located within the Mulatos District in Sonora, Mexico. PDA is a higher-grade underground deposit adjacent to the Mulatos open pit.

Given PDA’s attractive economics and proximity to the existing Mulatos infrastructure, the Company anticipates starting development of PDA in 2025 with first production expected mid-2027. The project is expected to nearly triple the mine life of the Mulatos District, extending production into 2035. There are excellent opportunities currently being tested that could extend the mine life further and enhance already robust economics through the significant exploration upside potential at both PDA and Cerro Pelon, as outlined earlier today.

PDA Project Highlights

- Average annual gold production of 127,000 ounces over the first four years and 104,000 ounces over the current mine life, based on Mineral Reserves as at December 31, 2023

- Low cost profile: total cash costs of $921 per payable ounce and mine-site all-in sustaining costs of $1,003 per payable ounce, consistent with the Company’s overall low cost structure

- Mine life tripled to 2035: PDA mine life of eight years based on current Mineral Reserves, extending the Mulatos District mine life from 2027 to 2035

- High-return project with significant upside potential

- After-tax Internal Rate of Return (“IRR”) of 46% and after-tax Net Present Value (“NPV”) (5%) of $269 million (using base case gold price assumption of $1,950 per ounce and a MXN/USD foreign exchange rate of 18:1)

- After-tax IRR of 73% and after-tax NPV (5%) of $492 million at current gold prices of approximately $2,500 per ounce and a MXN/USD foreign exchange rate of 18:1

- Payback of two years at the base case gold price of $1,950/oz and 1.5 years at current gold prices

- Low initial capital to be internally funded by strong ongoing free cash flow generation at the Mulatos District

- Initial capital of $165 million to be spent over a two-year period starting mid-2025. Life of mine capital is expected to total $231 million including $66 million of sustaining capital

- Low initial capital intensity of $195 per ounce produced, or $273 per ounce based on total life of mine capital

- PDA will benefit from the use of existing crushing and mill infrastructure from Cerro Pelon and Island Gold, supporting lower initial capital and project execution risk

- La Yaqui Grande is expected to finance the development of PDA at base case gold prices of $1,950 per ounce, following which PDA is expected to generate strong free cash flow. Through the first half of 2024, the Mulatos District generated $120 million of mine-site free cash flow

- Lower execution risk with PDA located within existing operation

- Experienced team in Mexico with strong track record of building projects on schedule and within budget including La Yaqui Phase I, Cerro Pelon and La Yaqui Grande

- PDA will represent the second underground mine developed and operated in the Mulatos District following San Carlos

- Lower development and permitting risk with PDA located within the existing operating footprint in the Mulatos District and utilizing existing infrastructure

- Significant exploration upside at PDA and Cerro Pelon

- Higher-grade mineralization continues to be extended beyond existing Mineral Reserves and Resources at PDA and the deposit remains open in multiple directions, highlighting the potential for further growth

- Higher-grade mineralization intersected below the past producing Cerro Pelon open pit which is expected to support an initial underground Mineral Resource with the year-end Mineral Reserve and Resource update to be released in February 2025. Cerro Pelon represents upside as a potential source of additional feed to the PDA sulphide mill that could extend the higher rates of production beyond the first four years of the current mine plan

“Mulatos has been operating for nearly 20 years reflecting a long-term track record of exploration success with the discovery of multiple new deposits in the District. PDA is an extension of that success, having discovered and outlined another attractive, high-return project that we expect will extend the Mulatos District mine life to at least 2035, representing 30 years since it began producing. The development of PDA and transition to underground sulphide milling operations will open up additional opportunities for growth in the Mulatos District. Given our ongoing exploration success at PDA, and newly defined and growing higher-grade zones of mineralization at Cerro Pelon, we see excellent potential to further extend the mine life and add to already attractive economics,” said John A. McCluskey, President and Chief Executive Officer.

| Puerto Del Aire Project Highlights | Life of Mine1 |

| Production | |

| Mine life (years) | 8 |

| Total gold production (000 ounces) | 848 |

| Total payable gold production (000 ounces) | 806 |

Average annual gold production (000 ounces) | |

| Years 1 to 4 | 127 |

| Years 1 to 8 | 104 |

| Total ore mined (000 tonnes) | 5,375 |

| Average gold grade mined (grams per tonne) | 5.61 |

| Average mill throughput (tonnes per day (“tpd”)) | 2,000 |

| Gold recovery (%) | 85% |

| Gold payability (%) | 95% |

| Operating Costs | |

| Mining cost per tonne of ore mined | $88 |

| Processing cost per tonne of ore milled | $20 |

| G&A cost per tonne of ore milled | $20 |

| Total site operating cost per tonne of ore milled | $120 |

| Total operating cost per tonne of ore milled (including concentrate treatment & transportation) | $127 |

| Total cash cost (per payable ounce)2 | $921 |

| Mine-site all-in sustaining cost (per payable ounce)2 | $1,003 |

| Capital Costs (millions) 1 | |

| Initial capital expenditure | $165 |

| Sustaining capital expenditure | $66 |

| Total capital expenditure | $231 |

| Initial capital intensity (per ounce produced) | $195 |

| Base Case Economic Analysis1 | |

| IRR (after-tax) | 46% |

| NPV @ 0% discount rate (millions, after-tax) | $383 |

| NPV @ 5% discount rate (millions, after-tax) | $269 |

| Gold price assumption (per payable ounce) | $1,950 |

| Exchange Rate (MXN/USD) | 18.0 |

| Economic Analysis at $2,500 per ounce Gold Price1 | |

| IRR (after-tax) | 73% |

| NPV @ 0% discount rate (millions, after-tax) | $676 |

| NPV @ 5% discount rate (millions, after-tax) | $492 |

| Gold price assumption (per payable ounce) | $2,500 |

| Exchange Rate (MXN/USD) | 18.0 |

1 Capital spending and economic analysis (NPV and IRR) are calculated starting January 1, 2025

2 Total cash costs and mine-site all-in sustaining costs include silver as a by-product credit, the 0.5% government royalty on revenue, and are per payable ounce

Mineral Reserves and Resources

The PDA mine plan and economic analysis are based on Mineral Reserves as of December 31, 2023 which total 5.4 million tonnes (“Mt”), grading 5.61 grams per tonne of gold (“g/t Au”), containing 969,000 ounces of gold. Additionally, the project hosts Measured and Indicated Mineral Resources which total 2.1 Mt, grading 3.54 g/t Au, containing 240,000 ounces of gold. Only Mineral Reserves were included in the mine plan with Mineral Resources representing potential upside.

Mineral Reserves – Effective as of December 31, 2023

| Classification | Tonnage (000’s) | Grade (g/t Au) | Contained oz (000’s Au) |

| Proven | 833 | 4.71 | 126 |

| Probable | 4,542 | 5.77 | 843 |

| Total Proven & Probable | 5,375 | 5.61 | 969 |

- Mineral Reserves reported are consistent with the CIM Definition Standards for Mineral Resources and Mineral Reserves.

- Mineral Reserves are reported to a cut-off grade of 3.0 g/t Au.

- The cut-off grades are based on a gold price of $1,400/oz Au.

- Metallurgical Au recovery is 85%.

- Totals may not add up due to rounding.

- Chris Bostwick, FAusIMM, Senior Vice President, Technical Services is the Qualified Person for the Mineral Reserve estimate. Mr. Bostwick is a Qualified Person within the meaning of Canadian Securities Administrator's National Instrument 43-101 ("NI 43-101").

Mineral Resources – Effective as of December 31, 2023

| Category | Tonnage (000’s) | Grade (g/t Au) | Contained oz (000’s Au) |

| Measured Indicated | 326 1,780 | 3.29 3.59 | 35 205 |

| Measured & Indicated | 2,106 | 3.54 | 240 |

| Inferred | 73 | 5.97 | 14 |

- Mineral Resources reported are consistent with the CIM Definition Standards for Mineral Resources and Mineral Reserves.

- The Mineral Resources are reported at an assumed gold price of US$1,600/oz.

- Mineral Resources are not Mineral Reserves and do not have demonstrated economic viability. There is no certainty that all or any part of the Mineral Resources estimated will be converted into Mineral Reserves.

- Contained Au ounces are in-situ and do not include metallurgical recovery losses.

- Mineral Resources are exclusive of Mineral Reserves.

- Totals may not add up due to rounding.

- Marc Jutras P.Eng., Principal, Ginto Consulting Inc. is the Qualified Person for the Mineral Resource estimate. Mr. Jutras is a Qualified Person within the meaning of Canadian Securities Administrator's National Instrument 43-101 ("NI 43-101").

Economic Analysis

PDA’s estimated after-tax IRR is 46% and after-tax NPV (5%) is $269 million assuming a gold price of $1,950 per payable ounce and MXN/USD foreign exchange rate of 18:1. Assuming spot gold prices of approximately $2,500 per ounce and MXN/USD foreign exchange rate of 18:1, the after-tax IRR increases to 73% and after-tax NPV (5%) increases to $492 million.

The mine plan, operating parameters, and capital estimates incorporated in the study are based on actual operating experience, and mining contractor quotations. Capital estimates for the processing circuit are based on Class 5 estimates from the third-party engineering firm that designed the processing circuit at La Yaqui Grande.

The project economics are sensitive to metal price assumptions, foreign exchange rates, and input costs as detailed in the tables below.

Puerto Del Aire After-Tax NPV (5%) Sensitivity ($ Millions)

| -10% | -5% | Base Case | 5% | 10% | ||

| Gold Price | $190 | $230 | $269 | $309 | $348 | |

| Mexican Peso | $288 | $279 | $269 | $258 | $245 | |

| Operating Costs | $305 | $287 | $269 | $251 | $233 | |

| Capital Costs | $286 | $277 | $269 | $261 | $252 | |

Puerto Del Aire After-Tax NPV (5%) Sensitivity to Gold Price and MXN/USD ($ Millions)

| Mexican Peso | ||||||

| Gold Price US$/oz | 17.0 | 18.0 | 19.0 | 20.0 | ||

| $1,750 | $175 | $188 | $199 | $209 | ||

| $1,850 | $216 | $229 | $240 | $250 | ||

| $1,950 | $257 | $269 | $280 | $290 | ||

| $2,100 | $317 | $330 | $341 | $351 | ||

| $2,300 | $398 | $411 | $422 | $432 | ||

| $2,500 | $480 | $492 | $503 | $513 | ||

Puerto Del Aire After-Tax IRR Sensitivity to Gold Price and MXN/USD (%)

| Mexican Peso | ||||||

| Gold Price US$/oz | 17.0 | 18.0 | 19.0 | 20.0 | ||

| $1,750 | 33.3% | 35.6% | 37.7% | 39.7% | ||

| $1,850 | 38.8% | 41.1% | 43.2% | 45.2% | ||

| $1,950 | 44.0% | 46.3% | 48.5% | 50.5% | ||

| $2,100 | 51.4% | 53.9% | 56.1% | 58.1% | ||

| $2,300 | 60.9% | 63.4% | 65.7% | 67.9% | ||

| $2,500 | 69.9% | 72.5% | 74.9% | 77.2% | ||

Project Overview

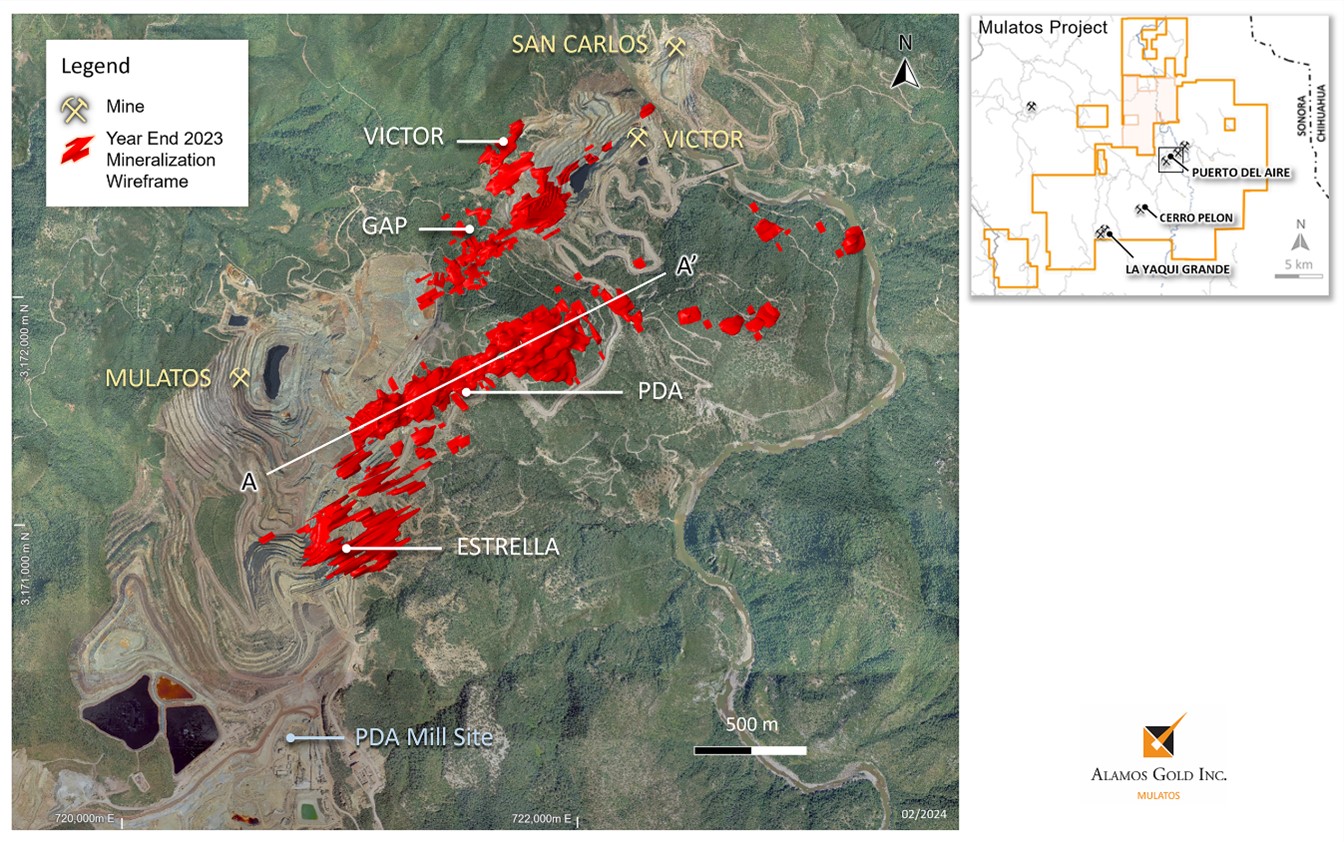

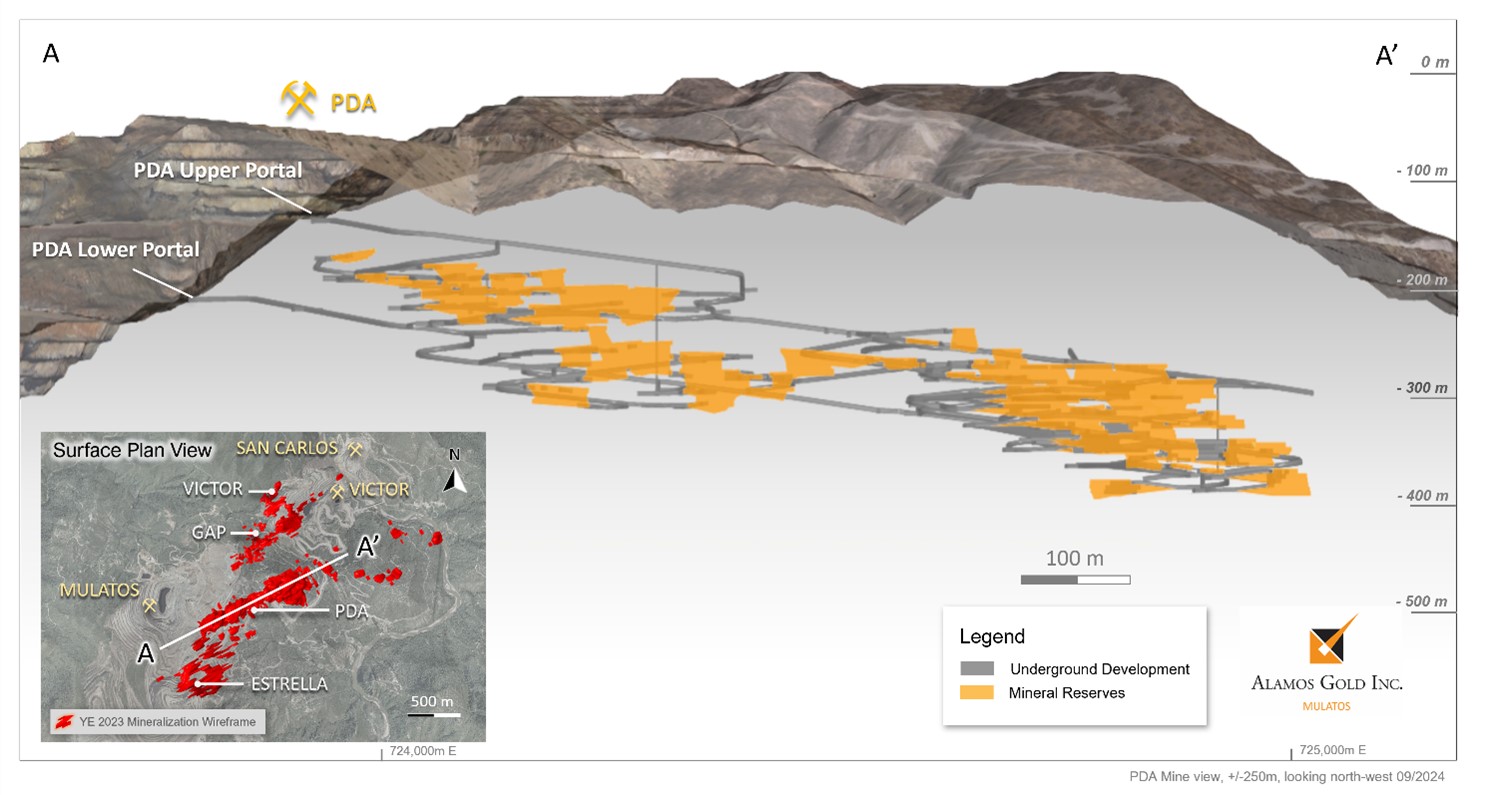

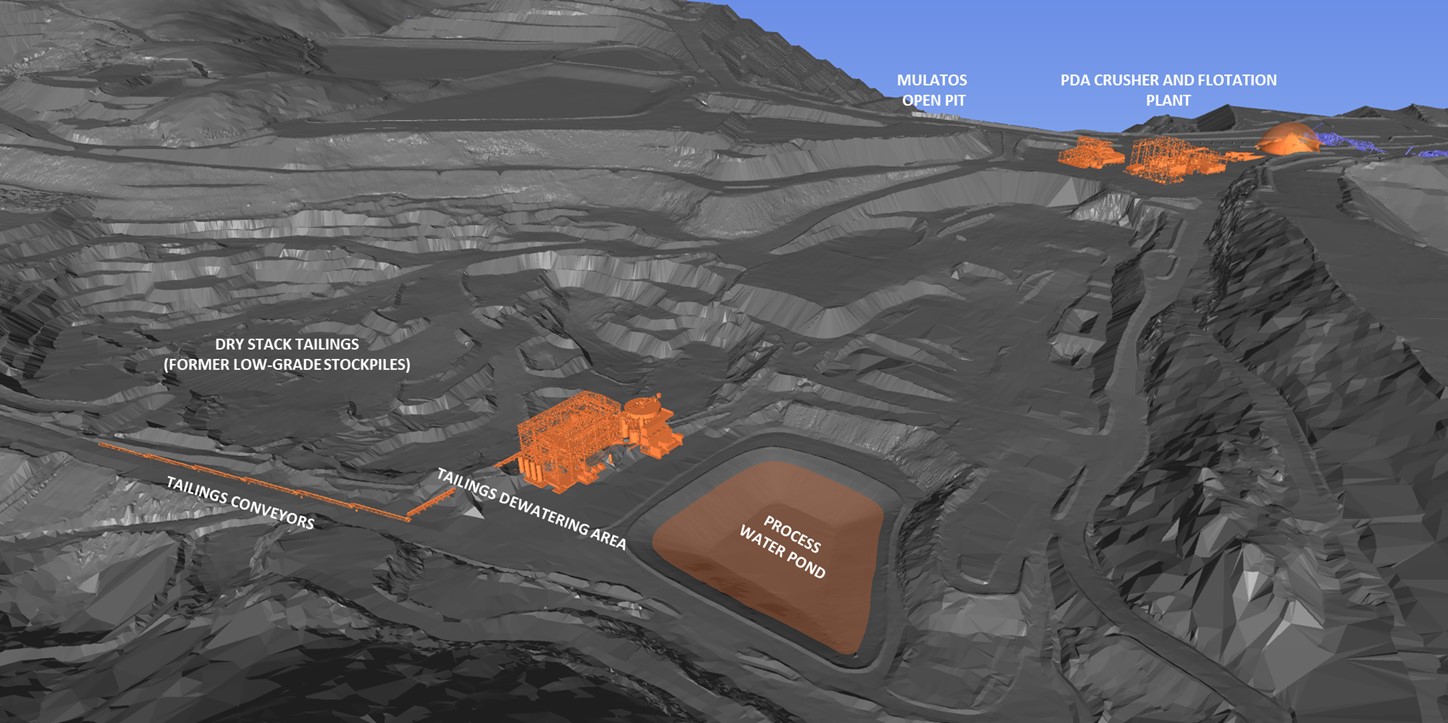

The PDA underground deposit is located adjacent to the main Mulatos pit and will be accessed via two portals located in the east wall of the Mulatos Pit (Figures 1 and 2). Underground ore mined will be processed through a flotation plant. No cyanide will be utilized with a concentrate produced for final gold recovery offsite. Tailings from onsite processing will be dry stacked.

Higher-grade sulphide mineralization was intersected at PDA more than 10 years ago. The focus at that time was on finding additional oxide, heap leachable ore such that follow up drilling at PDA did not resume until 2019. The exploration program has been extremely successful with an initial Mineral Reserve of 428,000 ounces (2.8 Mt grading 4.67 g/t Au) declared at the end of 2021. Since then, the deposit has continued to grow, more than doubling by the end of 2023 to 1.0 million ounces with grades also increasing 20% (5.4 Mt grading 5.61 g/t Au).

PDA will represent the second underground mining operation within the Mulatos District following San Carlos underground which successfully operated from 2014 to 2018. PDA will be developed by an experienced team with a strong track record of building projects on schedule and within budget including La Yaqui Phase I, Cerro Pelon, and most recently La Yaqui Grande.

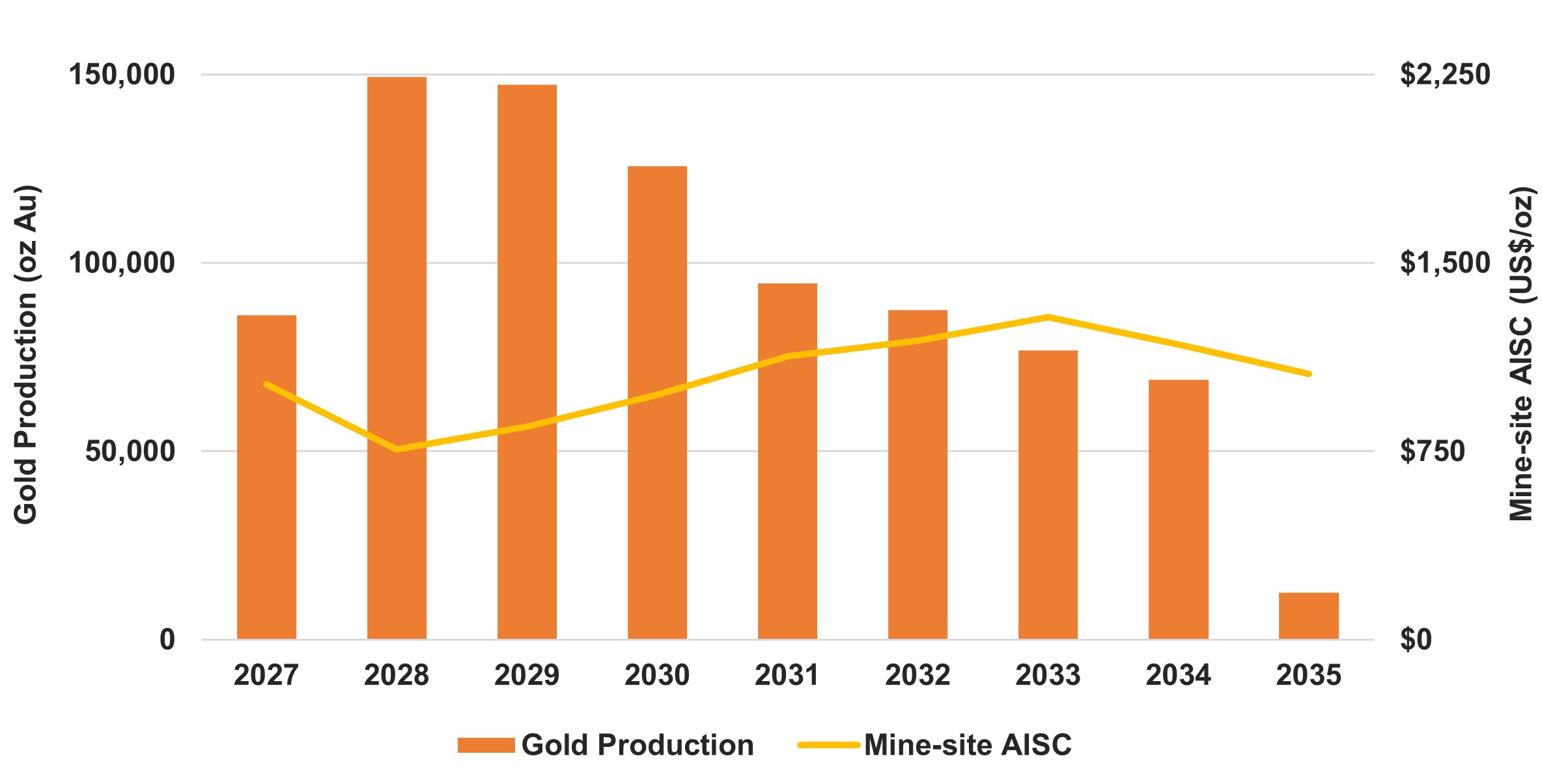

Production and Mine-Site AISC Profile

Mining

PDA will be accessed via two portals located in the east wall of the Mulatos Pit. Transverse long-hole open stoping will be the primary mining method utilized, as well as underhand drift and fill, with cemented rockfill supporting higher mining and ore recovery rates. Ore will be mined at a rate of 2,000 tonnes per day (“tpd”) over an eight-year mine life based on existing Mineral Reserves. Contract mining will be utilized over the mine life.

Initial production from PDA is expected mid-2027. Grades mined are expected to average approximately 7 g/t Au over the first four years supporting higher average annual production of 127,000 ounces over that time frame, and peak annual production of 149,000 ounces

Grades are expected to decrease to average approximately 4 g/t Au 2031 onward under the current mine plan. Ongoing exploration success at PDA and Cerro Pelon represents an upside opportunity to define additional higher-grade Mineral Reserves and Resources that could maintain higher grades and production well beyond the initial four years of the current mine plan.

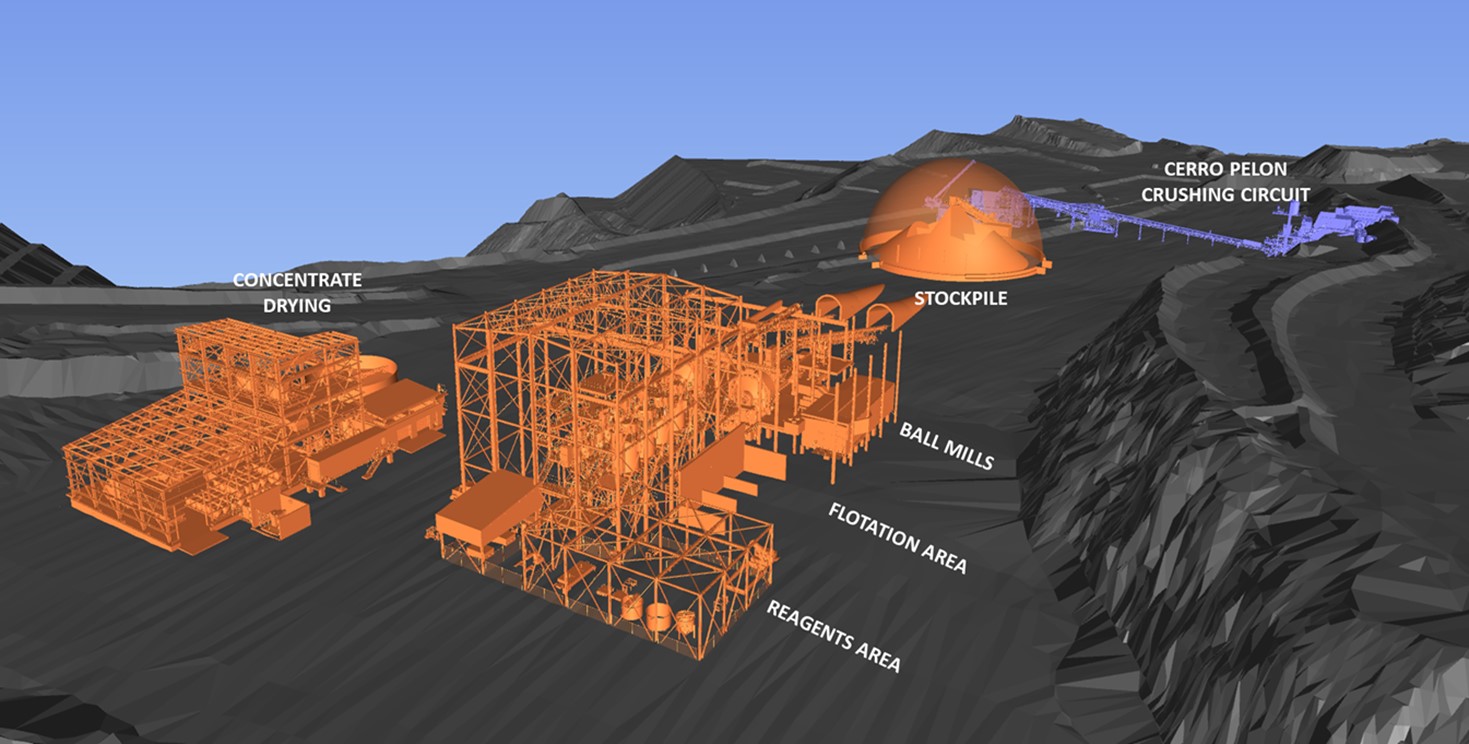

Processing

The processing circuit will include three-stage crushing, utilizing the existing Cerro Pelon crushing circuit, and two primary ball mills. One of the ball mills will come from Island Gold as the mill will be decommissioned in 2025 with ore from Island Gold to be fed through the larger Magino mill. Ore at PDA will be crushed to 80% passing (P80) ¼ inch. Following crushing, ore will be sent to the grinding circuit and then flotation circuit that includes both rougher flotation and cleaner flotation (Figures 3 and 4).

The flow sheet incorporates the following major process operations:

- Three-stage crushing

- Two ball mills in parallel – one to be supplied from the Island Gold mill

- Two regrind mills – supplied from the Island Gold mill

- Flotation circuit

- Concentrate dewatering

- Tailings dewatering

A concentrate will be produced with gold to be recovered off-site, eliminating the use of cyanide for on-site processing. Over the life of mine, approximately 300,000 tonnes of concentrate will be produced at average grades of 90 g/t Au. Off-site treatment, refining and transportation costs are estimated to be $130 per tonne of concentrate. Mill recoveries are expected to average 85%, of which 95% is payable.

Power to site will be supplied from the existing connection to the commercial electricity grid operated by the state-owned electric utility of Mexico, the Comisión Federal de Electricidad (“CFE”).

With the tailings dry stacked, no tailings dam will be required. Tailings will be filtered and deposited where low-grade stockpiles from Mulatos were previously located.

Operating Costs

Total cash costs are expected to average $921 per payable ounce and mine-site all-in sustaining costs $1,003 per payable ounce over the life of the operation. Total unit operating costs are expected to average $127 per tonne of ore milled, including concentrate treatment and transportation costs. This includes average mining costs of $88 per tonne of ore mined, processing costs of $20 per tonne of ore milled, and G&A costs of $20 per tonne of ore milled.

The breakdown of unit costs is summarized as follows.

| Operating Costs1 | US$/t | LOM US$M | |

| Mining | $/t mined | $88 | $473 |

| Processing | $/t milled | $20 | $117 |

| G&A | $/t milled | $20 | $117 |

| Total On-Site Operating Costs | $/t milled | $120 | $707 |

| Concentrate Treatment & Transportation | $/t conc. | $130 | $38 |

| Total Operating Costs | $/t milled | $127 | $746 |

| Total Cash Costs2.3 | $/oz | $921 | |

| Mine-site All-in Sustaining Costs2.3 | $/oz | $1,003 |

1 Operating costs exclude silver by-product credit, 0.5% government royalty on revenue and working capital

2 Total cash costs and mine-site all-in sustaining costs include silver as a by-product credit, the 0.5% government royalty on revenue, and are per payable ounce

3 Please refer to the Cautionary Notes on non-GAAP Measures and Additional GAAP Measures

Capital Costs

Total initial capital is estimated to be $165 million and expected to be spent over a two-year period starting mid-2025. This includes $51 million for underground development, and $109 million for the processing facility which includes a 25% contingency.

The crushing circuit that was previously utilized for Cerro Pelon will be re-located and integrated into the PDA circuit, and one primary ball mill and two regrind mills from Island Gold will be refurbished and shipped to site. The remaining life of mine capital includes $66 million of sustaining capital, predominantly for underground development.

A breakdown of the initial and total capital requirements is detailed as follows.

| Capital Cost ($ millions) | |

| Processing Facility1 | $109 |

| Mine Development & Fixed Assets | $56 |

| Total Initial Capital | $165 |

| Sustaining capital | $66 |

| Total Capital | $231 |

1 Includes a 25% contingency

Taxes and Royalties

Earnings at PDA are subject to the corporate tax rate of 30%, as well as the Mexican Mining Royalty (7.5% EBITDA royalty). Additionally, the project is subject to the 0.5% government royalty on revenue. The Mulatos District, including PDA is not subject to any third party royalties. Over the current mine life and using a base case gold price assumption of $1,950 per ounce, PDA is expected to pay $215 million in taxes.

Permitting

An amendment to the existing environmental impact assessment (“MIA”) will be required for PDA. The amended MIA application has been submitted with approval expected by the end of 2024. PDA is expected to be a straightforward project to permit given:

- PDA will be an underground mine located next to the Mulatos pit, within the existing Mulatos District concessions

- No Change of Land Use (“CUS”) permit is expected to be required with PDA located within the existing Mulatos operating footprint

- No tailings dam will be required with dry stacked tailings

- No use of cyanide with a concentrate to be produced and shipped off-site for treatment

Additional Upside Opportunities

Addition of a paste plant

The addition of a paste plant will be evaluated as an upside opportunity. The use of paste backfill would allow for increased mining recovery, contributing to higher life of mine production, as well as faster stope cycle times providing improved operational flexibility.

Ongoing near-mine exploration success at PDA

Through ongoing exploration success, PDA’s Mineral Reserves base had increased to 1.0 million ounces (5.4 mt grading 5.61 g/t Au) at the end of 2023, more than doubling over the previous two years with grades also increasing 20%. This growth to the end of 2023 was incorporated into the PDA development plan.

The initial focus of the surface exploration program in 2024 has been on the GAP-Victor zones, and in the relatively untested area between the PDA zones and Gap-Victor. The program has been successful in further extending high-grade gold mineralization beyond Mineral Reserves and Resources. Given ongoing exploration success in 2024, and with the deposit open in multiple directions, there is excellent potential for further growth in higher-grade Mineral Reserves and Resources which represents upside to the project.

New highlights reported earlier today include1:

GAP-Victor Zone

- 5.43 g/t Au over 18.05 m (23MUL278);

- 23.60 g/t Au over 3.00 m (24MUL302);

- 27.62 g/t Au (23.06 g/t cut) over 2.25 m (24MUL332);

- 12.28 g/t Au over 4.95 m (24MUL363); and

- 5.77 g/t Au over 8.65 m (24MUL304).

PDA3 Zone

- 3.03 g/t Au over 28.40m (24MUL347); and

- 6.63 g/t Au over 5.50 m (24MUL365).

PDA Extension Zone

- 36.20 g/t Au over 0.90 m (24MUL341);

- 3.51 g/t Au over 5.05 m (24MUL315); and

- 4.16 g/t Au over 4.20 m (24MUL283).

1All reported composite widths are estimated true width of the mineralized zones. Drillhole composite gold grades reported as “cut” at PDA include higher grade samples which have been cut to 40 g/t Au.

Cerro Pelon and other regional targets

Cerro Pelon was an open pit operation that successfully operated between 2019 and 2021 with 127,000 ounces of gold produced at an average grade of 1.7 g/t Au. Open pit oxide ore was trucked from the Cerro Pelon pit to the existing Mulatos crushing and heap leach infrastructure, which included a dedicated Cerro Pelon crushing plant.

Between 2008 and 2017 high-grade mineralization was intersected below the Cerro Pelon pit across multiple drill holes including the following previously reported highlights from 2015 and 20162:

- 15.35 g/t Au (14.04 g/t cut) over 25.04 m (15PEL012);

- 9.16 g/t Au over 19.22 m (16PEL018);

- 10.36 g/t Au over 17.40 m (15PEL020);

- 6.95 g/t Au over 13.53 m (15PEL069); and

- 13.47 g/t Au over 3.47 m (15PEL085).

2All reported historic composite widths are estimated true width of the mineralized zones. Drillhole composite gold grades reported as “cut” include higher grade samples which have been cut to 40 g/t Au.

The 2024 drill program at Cerro Pelon has expanded high-grade mineralization beyond the historical drilling in multiple oxide and sulphide zones. Step-out drilling below the open pit has identified significant high-grade feeder structures that range in size from 45 to 125 metres (“m”) in width and up to 170 m vertically. New highlights reported earlier today include1:

- 5.45 g/t Au over 27.90 m, including 31.07 g/t Au over 1.25 m (24PEL048);

- 12.47 g/t Au (9.41 g/t cut) over 6.46 m, including 58.10 g/t Au (40.00 g/t cut) over 1.09 m (24PEL048);

- 4.79 g/t Au over 15.82 m (24PEL071);

- 4.46 g/t Au over 15.40 m (24PEL051);

- 5.64 g/t Au over 12.16 m (24PEL059);

- 5.77 g/t Au over 9.81 m (24PEL067); and

- 4.01 g/t Au over 13.85 m (24PEL054).

1All reported composite widths are estimated true width of the mineralized zones. Drillhole composite gold grades reported as “cut” at Cerro Pelon include higher grade samples which have been cut to 40 g/t Au.

Drilling to date indicates that more than five pipes with lateral dimensions ranging from 150 m by 100 m, to 75 m by 60 m, and vertical extents ranging between 40 m and 150 m. There is significant potential to expand the mineralization in all directions with limited drilling completed beyond the five feeders identified to date.

Cerro Pelon is located nine kilometres (“km”) by road from the planned PDA mill, similar to the distance that lower grade open pit ore from Cerro Pelon was trucked to the Mulatos circuit (Figure 5). An initial underground Mineral Resource is expected to be declared on Cerro Pelon with the 2024 year-end update which will be evaluated as a source of additional high-grade mill feed.

Under the current PDA mine plan, grades are expected to decrease from 2031 onward. Cerro Pelon represents an opportunity to mine and process higher relative grades, extending higher rates of gold production beyond the first four years of the current mine plan.

Technical Disclosure

Chris Bostwick, FAusIMM, Alamos Gold's Senior Vice President, Technical Services, has reviewed and approved the scientific and technical information contained in this news release. Mr. Bostwick is a Qualified Person within the meaning of Canadian Securities Administrator's National Instrument 43-101 ("NI 43-101").

About Alamos

Alamos is a Canadian-based intermediate gold producer with diversified production from three operating mines in North America. This includes the Young-Davidson mine and Island Gold District in northern Ontario, Canada and the Mulatos District in Sonora State, Mexico. Additionally, the Company has a significant portfolio of development stage projects, including the Phase 3+ Expansion at Island Gold, and the Lynn Lake project in Manitoba, Canada. Alamos employs more than 2,400 people and is committed to the highest standards of sustainable development. The Company’s shares are traded on the TSX and NYSE under the symbol “AGI”.

FOR FURTHER INFORMATION, PLEASE CONTACT:

Scott K. Parsons

Senior Vice President, Corporate Development & Investor Relations

(416) 368-9932 x 5439

The TSX and NYSE have not reviewed and do not accept responsibility for the adequacy or accuracy of this release.

Cautionary Note Regarding Forward Looking Statements

Cautionary Note

This news release contains or incorporates by reference “forward-looking statements” and “forward-looking information” as defined under applicable Canadian and U.S. securities laws. All statements in this news release, other than statements of historical fact, which address events, results, outcomes or developments that the Company expects to occur are, or may be deemed to be, forward-looking statements and are generally, but not always, identified by the use of forward-looking terminology such as "expect", “assume”, “anticipate”, “potential”, “plan”, “opportunity”, “estimate”, “continue”, “ongoing”, “evaluate”, “budget”, “target” or variations of such words and phrases and similar expressions or statements that certain actions, events or results “may", “could”, “would”, "might" or "will" be taken, occur or be achieved or the negative connotation of such terms. Forward-looking statements contained in this news release are based on information, expectations, estimates and projections as of the date of this news release.

Forward-looking statements in this news release include, but may not be limited to, information as to strategy, plans, expectations or future financial or operating performance pertaining to, or anticipated to result from, the PDA development project, such as expectations, assumptions and estimations regarding: the project and its attractive economics and significant exploration upside; development of the project; the mine plan; the method of mining the project and the intended method of processing ore from the PDA deposit; initial underground Mineral Resource at Cerro Pelon; expected timing of approval of the amended MIA application for the PDA project; mine life and expected mine life extension at Mulatos; exploration potential, programs and targets; anticipated production; gold grades; mineralization; Mineral Reserves and Resources (and potential growth in Mineral Reserves as exploration continues); Proven and Probable Mineral Reserves; Inferred Mineral Resources; operating costs including mine-site all-in sustaining costs; capital costs; capital costs; economic analysis including anticipated after-tax net present value and internal rate of return; applicable taxes; gold price, other metal prices and foreign exchange rates; project execution risk; returns to stakeholders; and other statements that express management's expectations or estimates of future performance, operational, geological or financial results.

Exploration results that include geophysics, sampling, and drill results on wide spacings may not be indicative of the occurrence of a mineral deposit. Such results do not provide assurance that further work will establish sufficient grade, continuity, metallurgical characteristics and economic potential to be classed as a category of Mineral Resource. A Mineral Resource that is classified as "Inferred" or "Indicated" has a great amount of uncertainty as to its existence and economic and legal feasibility. It cannot be assumed that any or part of an "Indicated Mineral Resource" or "Inferred Mineral Resource" will ever be upgraded to a higher category of Mineral Resource. Investors are cautioned not to assume that all or any part of mineral deposits in these categories will ever be converted into Proven and Probable Mineral Reserves.

The Company cautions that forward-looking statements are necessarily based upon several factors and assumptions that, while considered reasonable by management at the time of making such statements, are inherently subject to significant business, economic, technical, legal, political, and competitive uncertainties, and contingencies. Known and unknown factors could cause actual results to differ materially from those projected in the forward-looking statements, and undue reliance should not be placed on such statements and information.

Such factors include (without limitation): the actual results of current exploration activities; conclusions of economic and geological evaluations; changes in project parameters as plans continue to be refined; any impacts of any illnesses, diseases, epidemics or pandemics on operations and the broader market, including the nature and duration of any regulatory responses; state and federal orders or mandates (including with respect to mining operations generally or auxiliary businesses or services required for the Company’s operations) in Mexico; changes in national and local government legislation, controls or regulations; failure to comply with environmental and health and safety laws and regulations; labour and contractor availability (and being able to secure the same on favourable terms); ability to sell or deliver gold doré bars; disruptions in the maintenance or provision of required infrastructure and information technology systems; fluctuations in the price of gold or certain other commodities such as, diesel fuel, natural gas, and electricity; operating or technical difficulties in connection with mining or development activities, including geotechnical challenges and changes to production estimates (which assume accuracy of projected ore grade, mining rates, recovery timing and recovery rate estimates and may be impacted by unscheduled maintenance); changes in foreign exchange rates (particularly the Canadian dollar, U.S. dollar, and Mexican peso); the impact of inflation; employee and community relations; litigation and administrative proceedings; disruptions affecting operations; availability of and increased costs associated with mining inputs and labour; delays in the development or updating of mine and/or development plans; delays in receiving approval of the amended MIA application for the PDA project; changes that may be required to the intended method of accessing and mining the deposit at Puerto Del Aire and changes related to the intended method of processing any ore from the deposit at Puerto Del Aire; inherent risks and hazards associated with mining and mineral processing including environmental hazards, industrial accidents, unusual or unexpected formations, pressures and cave-ins; the risk that the Company’s mines may not perform as planned; uncertainty with the Company's ability to secure additional capital to execute its business plans; the speculative nature of mineral exploration and development, risks in obtaining and maintaining necessary licenses, permits and authorizations, contests over title to properties; expropriation or nationalization of property; political or economic developments in Canada or Mexico and other jurisdictions in which the Company may carry on business in the future; increased costs and risks related to the potential impact of climate change; the costs and timing of construction and development of new deposits; risk of loss due to sabotage, protests and other civil disturbances; the impact of global liquidity and credit availability and the values of assets and liabilities based on projected future cash flows; and business opportunities that may be pursued by the Company.

For a more detailed discussion of such risks and other risk factors that may affect the Company's ability to achieve the expectations set forth in the forward-looking statements contained in this news release, see the Company’s latest 40-F/Annual Information Form and Management’s Discussion and Analysis, each under the heading “Risk Factors” available on the SEDAR website at www.sedarplus.ca or on EDGAR at www.sec.gov. The foregoing should be reviewed in conjunction with the information, risk factors and assumptions found in this news release.

The Company disclaims any intention or obligation to update or revise any forward-looking statements whether as a result of new information, future events or otherwise, except as required by applicable law.

Cautionary Note to U.S. Investors

Alamos prepares its disclosure in accordance with the requirements of securities laws in effect in Canada. Unless otherwise indicated, all Mineral Resource and Mineral Reserve estimates included in this document have been prepared in accordance with Canadian National Instrument 43-101 - Standards of Disclosure for Mineral Projects (“NI 43-101”) and the Canadian Institute of Mining, Metallurgy and Petroleum (the “CIM”) - CIM Definition Standards on Mineral Resources and Mineral Reserves, adopted by the CIM Council, as amended (the “CIM Standards”). NI 43-101 is a rule developed by the Canadian Securities Administrators, which established standards for all public disclosure an issuer makes of scientific and technical information concerning mineral projects. Mining disclosure in the United States was previously required to comply with SEC Industry Guide 7 (“SEC Industry Guide 7”) under the United States Securities Exchange Act of 1934, as amended. The U.S. Securities and Exchange Commission (the “SEC”) has adopted final rules, to replace SEC Industry Guide 7 with new mining disclosure rules under sub-part 1300 of Regulation S-K of the U.S. Securities Act (“Regulation S-K 1300”) which became mandatory for U.S. reporting companies beginning with the first fiscal year commencing on or after January 1, 2021. Under Regulation S-K 1300, the SEC now recognizes estimates of “Measured Mineral Resources”, “Indicated Mineral Resources” and “Inferred Mineral Resources”. In addition, the SEC has amended its definitions of “Proven Mineral Reserves” and “Probable Mineral Reserves” to be substantially similar to international standards.

Investors are cautioned that while the above terms are “substantially similar” to CIM Definitions, there are differences in the definitions under Regulation S-K 1300 and the CIM Standards. Accordingly, there is no assurance any mineral reserves or mineral resources that the Company may report as “proven mineral reserves”, “probable mineral reserves”, “measured mineral resources”, “indicated mineral resources” and “inferred mineral resources” under NI 43-101 would be the same had the Company prepared the mineral reserve or mineral resource estimates under the standards adopted under Regulation S-K 1300. U.S. investors are also cautioned that while the SEC recognizes “measured mineral resources”, “indicated mineral resources” and “inferred mineral resources” under Regulation S-K 1300, investors should not assume that any part or all of the mineralization in these categories will ever be converted into a higher category of mineral resources or into mineral reserves. Mineralization described using these terms has a greater degree of uncertainty as to its existence and feasibility than mineralization that has been characterized as reserves. Accordingly, investors are cautioned not to assume that any measured mineral resources, indicated mineral resources, or inferred mineral resources that the Company reports are or will be economically or legally mineable.

Cautionary non-GAAP Measures and Additional GAAP Measures

Note that for purposes of this section, GAAP refers to IFRS. The Company believes that investors use certain non-GAAP and additional GAAP measures as indicators to assess gold mining companies. They are intended to provide additional information and should not be considered in isolation or as a substitute for measures of performance prepared with GAAP.

“Cash flow from operating activities before changes in non-cash working capital” is a non-GAAP performance measure that could provide an indication of the Company’s ability to generate cash flows from operations and is calculated by adding back the change in non-cash working capital to “cash provided by (used in) operating activities” as presented on the Company’s consolidated statements of cash flows. “Cash flow per share” is calculated by dividing “cash flow from operations before changes in working capital” by the weighted average number of shares outstanding for the period. “Free cash flow” is a non-GAAP performance measure that is calculated as cash flows from operations net of cash flows invested in mineral property, plant and equipment and exploration and evaluation assets as presented on the Company’s consolidated statements of cash flows and that would provide an indication of the Company’s ability to generate cash flows from its mineral projects. “Mine site free cash flow” is a non-GAAP measure which includes cash flow from operating activities at, less capital expenditures at each mine site. “Return on equity” is defined as earnings from continuing operations divided by the average total equity for the current and previous year. “Mining cost per tonne of ore” and “cost per tonne of ore” are non-GAAP performance measures that could provide an indication of the mining and processing efficiency and effectiveness of the mine. These measures are calculated by dividing the relevant mining and processing costs and total costs by the tonnes of ore processed in the period. “Cost per tonne of ore” is usually affected by operating efficiencies and waste-to-ore ratios in the period. “Total capital expenditures per ounce produced” is a non-GAAP term used to assess the level of capital intensity of a project and is calculated by taking the total growth and sustaining capital of a project divided by ounces produced life of mine. “Total cash costs per ounce”, “all-in sustaining costs per ounce”, “mine-site all-in sustaining costs”, and “all-in costs per ounce” as used in this analysis are non-GAAP terms typically used by gold mining companies to assess the level of gross margin available to the Company by subtracting these costs from the unit price realized during the period. These non-GAAP terms are also used to assess the ability of a mining company to generate cash flow from operations. There may be some variation in the method of computation of these metrics as determined by the Company compared with other mining companies. In this context, “total cash costs” reflects mining and processing costs allocated from in-process and doré inventory and associated royalties with ounces of gold sold in the period. Total cash costs per ounce are exclusive of exploration costs. “All-in sustaining costs per ounce” include total cash costs, exploration, corporate and administrative, share based compensation and sustaining capital costs. “Mine-site all-in sustaining costs” include total cash costs, exploration, and sustaining capital costs for the mine-site, but exclude an allocation of corporate and administrative and share based compensation. “Adjusted net earnings” and “adjusted earnings per share” are non-GAAP financial measures with no standard meaning under IFRS. “Adjusted net earnings” excludes the following from net earnings: foreign exchange gain (loss), items included in other loss, certain non-reoccurring items, and foreign exchange gain (loss) recorded in deferred tax expense. “Adjusted earnings per share” is calculated by dividing “adjusted net earnings” by the weighted average number of shares outstanding for the period.

Additional GAAP measures that are presented on the face of the Company’s consolidated statements of comprehensive income and are not meant to be a substitute for other subtotals or totals presented in accordance with IFRS, but rather should be evaluated in conjunction with such IFRS measures. This includes “Earnings from operations”, which is intended to provide an indication of the Company’s operating performance and represents the amount of earnings before net finance income/expense, foreign exchange gain/loss, other income/loss, and income tax expense. Non-GAAP and additional GAAP measures do not have a standardized meaning prescribed under IFRS and therefore may not be comparable to similar measures presented by other companies. A reconciliation of historical non-GAAP and additional GAAP measures are detailed in the Company’s latest Management’s Discussion and Analysis available online on the SEDAR website at www.sedar.ca or on EDGAR at www.sec.gov and at www.alamosgold.com.

| Table 1: PDA Life of Mine Production Schedule | ||||||||||||

| LOM | 2025 | 2026 | 2027 | 2028 | 2029 | 2030 | 2031 | 2032 | 2033 | 2034 | 2035 | |

| Mining | ||||||||||||

| Tonnes Mined (000 tonnes) | 5,375 | 434 | 723 | 719 | 721 | 730 | 730 | 730 | 588 | - | ||

| Mined Grade (g/t Au) | 5.61 | 6.94 | 7.54 | 7.47 | 6.35 | 4.74 | 4.38 | 3.85 | 3.85 | - | ||

| Processing | ||||||||||||

| Tonnes Milled (000 tonnes)1 | 5,872 | 516 | 730 | 730 | 730 | 730 | 730 | 730 | 730 | 247 | ||

| Milled Grade (g/t Au) | 5.29 | 6.10 | 7.48 | 7.38 | 6.29 | 4.74 | 4.38 | 3.85 | 3.46 | 1.85 | ||

| Mill Recovery (% Au)2 | 85% | 85% | 85% | 85% | 85% | 85% | 85% | 85% | 85% | 85% | ||

| Gold Production (000 oz) | 848 | 86 | 149 | 147 | 126 | 95 | 87 | 77 | 69 | 12 | ||

| Payable Gold Production (000 oz)2 | 806 | 79 | 139 | 137 | 116 | 86 | 79 | 69 | 62 | 11 | ||

| Operating Costs | ||||||||||||

| Mining (US$/tonne mined) | $87 | $66 | $99 | $97 | $93 | $85 | $84 | $84 | $82 | - | ||

| Processing (US$/tonne milled) | $20 | $24 | $19 | $19 | $19 | $19 | $19 | $19 | $19 | $25 | ||

| G&A (US$/tonne milled) | $20 | $20 | $20 | $20 | $20 | $20 | $20 | $20 | $20 | $20 | ||

| Total Cash Costs (US$/oz) 3,4 | $921 | $747 | $743 | $743 | $841 | $1,056 | $1,132 | $1,284 | $1,174 | $1,058 | ||

| Mine-Site All-in Sustaining Costs (US$/oz) 3,4 | $1,003 | $1,016 | $758 | $848 | $974 | $1,129 | $1,189 | $1,284 | $1,174 | $1,058 | ||

| Capital Expenditures | ||||||||||||

| Initial Capital (US$M) | $165 | $20 | $93 | $52 | - | - | - | - | - | - | - | - |

| Sustaining Capital (US$M) | $66 | - | - | $22 | $2 | $15 | $16 | $7 | $5 | - | - | - |

| Total Capital (US$M) | $231 | $20 | $93 | $74 | $2 | $15 | $16 | $7 | $5 | - | - | - |

1 Processed tonnes exceed mined tonnes and Mineral Reserves reflecting the inclusion of lower grade development ore

2 Mill recoveries are expected to average 85% of which 95% are payable

3 Please refer to Cautionary Notes on non-GAAP Measures and Additional GAAP Measures

4 Total cash costs and mine-site all-in sustaining costs are per payable ounce and inclusive of silver credits, government royalties, and concentrate treatment and transportation costs while unit operating costs are reported exclusive of these costs

Figure 1: PDA Deposit and Mill Location

Figure 2: PDA Long Section Including Planned Underground Development

Figure 3: PDA Crushing and Flotation Plant

Figure 4: PDA Project Layout

Figure 5: PDA and Cerro Pelon Location Map, Mulatos District

Photos accompanying this announcement are available at

https://www.globenewswire.com/NewsRoom/AttachmentNg/18faa915-6092-42ba-b22c-78d283020fea

https://www.globenewswire.com/NewsRoom/AttachmentNg/8dfdb773-dad8-4fb8-9fd5-f5734af7db7f

https://www.globenewswire.com/NewsRoom/AttachmentNg/d6a81dd6-e621-48c9-80a7-1104a7d48152

https://www.globenewswire.com/NewsRoom/AttachmentNg/d3e2415b-81ac-41d4-9d4f-fcd7a9ba188c

https://www.globenewswire.com/NewsRoom/AttachmentNg/be9c547c-067b-4db5-ac8f-84d9b294e0ab

https://www.globenewswire.com/NewsRoom/AttachmentNg/92100ea6-66a8-48f4-afaf-93ffe91f257b

![]()