Matthews has followed the market’s trajectory closely, rising in tandem with the S&P 500 over the past six months. The stock has climbed by 10.6% to $30.45 per share while the index has gained 13.5%.

Is there a buying opportunity in Matthews, or does it present a risk to your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.We're cautious about Matthews. Here are three reasons why we avoid MATW and a stock we'd rather own.

Why Do We Think Matthews Will Underperform?

Originally a death care company, Matthews International (NASDAQ:MATW) is a diversified company offering ceremonial services, brand solutions and industrial technologies.

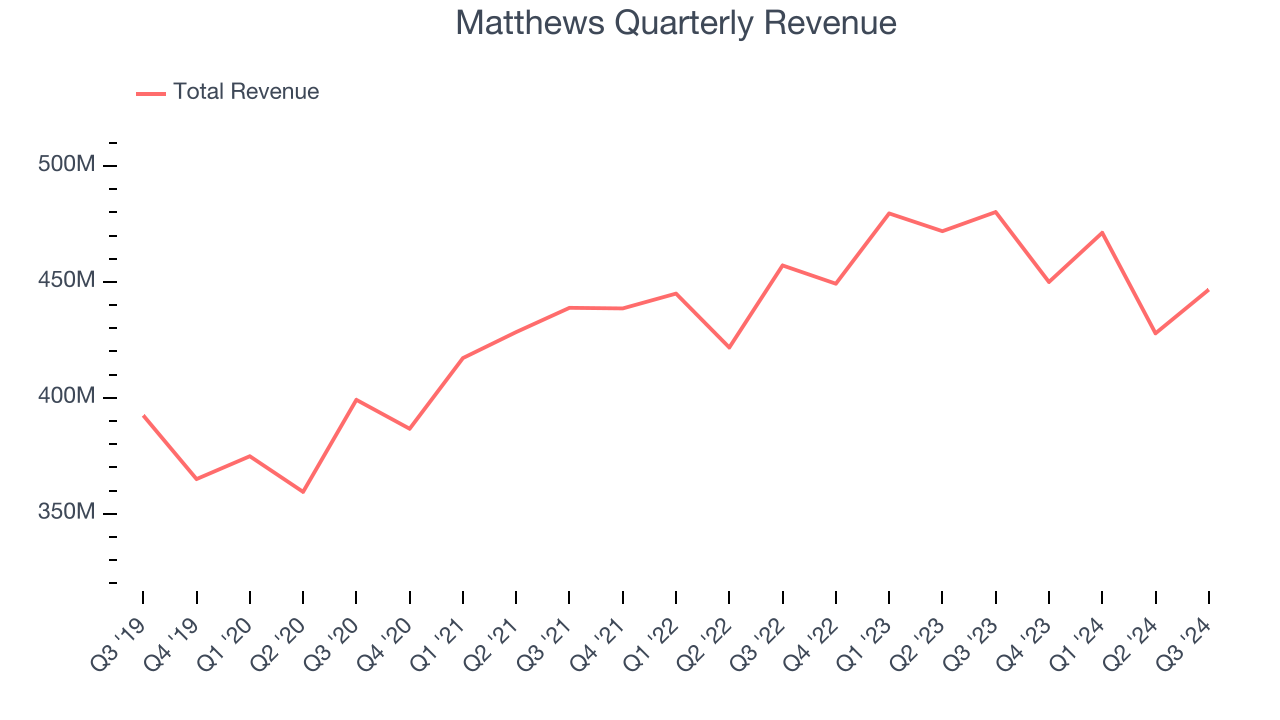

1. Long-Term Revenue Growth Disappoints

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last five years, Matthews grew its sales at a sluggish 3.2% compounded annual growth rate. This was below our standard for the consumer discretionary sector.

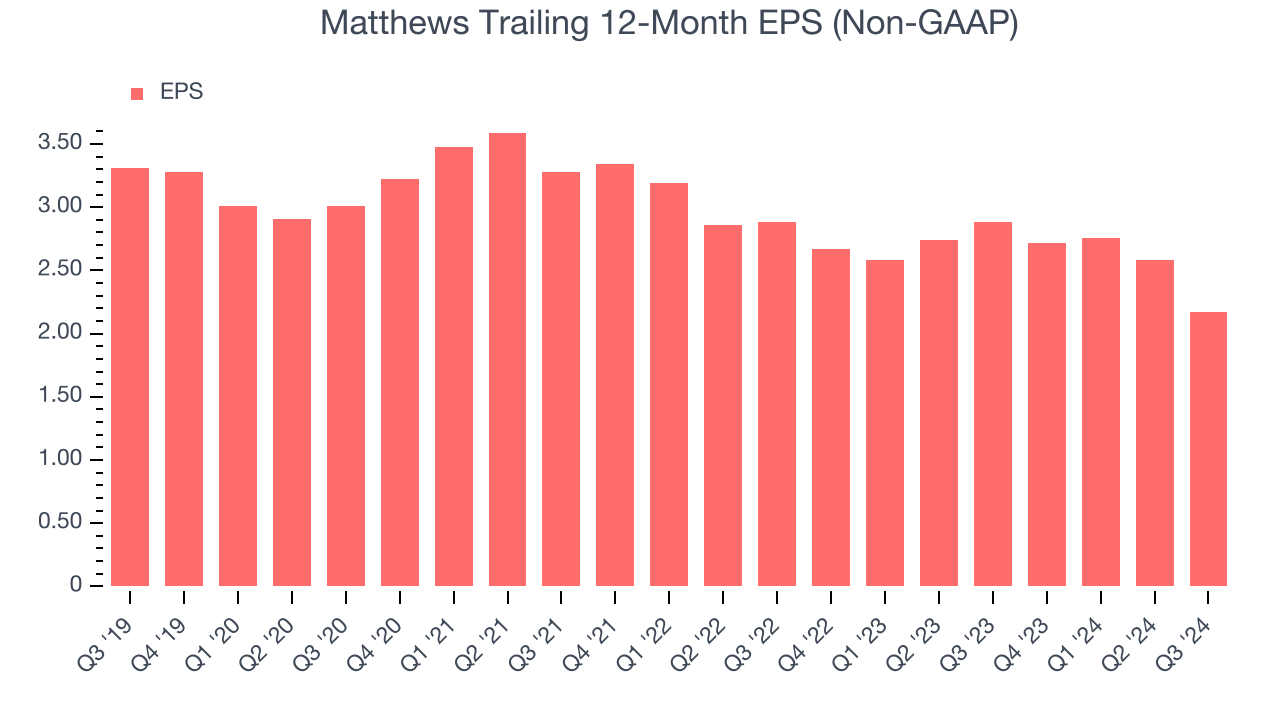

2. EPS Trending Down

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Sadly for Matthews, its EPS declined by 8.1% annually over the last five years while its revenue grew by 3.2%. This tells us the company became less profitable on a per-share basis as it expanded.

3. Projected Revenue Growth Shows Limited Upside

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Matthews’s revenue to stall, a slight deceleration versus its flat sales for the past two years. This projection doesn't excite us and suggests its products and services will face some demand challenges.

Final Judgment

Matthews falls short of our quality standards. That said, the stock currently trades at 20.3× forward price-to-earnings (or $30.45 per share). While this valuation is reasonable, we don’t see a big opportunity at the moment. There are better investments elsewhere. We’d suggest looking at Google, whose cloud computing and YouTube divisions are firing on all cylinders.

Stocks We Like More Than Matthews

With rates dropping, inflation stabilizing, and the elections in the rearview mirror, all signs point to the start of a new bull run - and we’re laser-focused on finding the best stocks for this upcoming cycle.

Put yourself in the driver’s seat by checking out our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,691% between September 2019 and September 2024) as well as under-the-radar businesses like United Rentals (+550% five-year return). Find your next big winner with StockStory today for free.