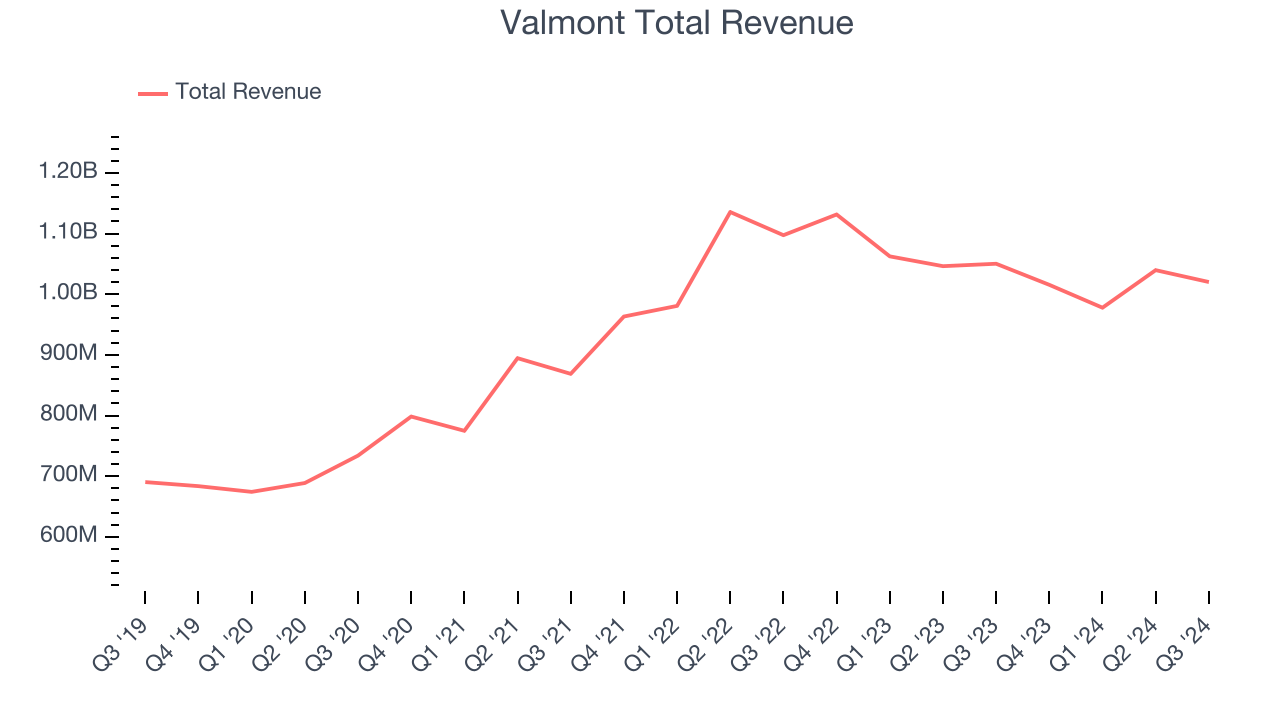

Infrastructure and agriculture equipment manufacturer Valmont Industries (NYSE:VMI) met Wall Street’s revenue expectations in Q3 CY2024, but sales fell 2.9% year on year to $1.02 billion. Its GAAP profit of $4.11 per share was 2.8% above analysts’ consensus estimates.

Is now the time to buy Valmont? Find out by accessing our full research report, it’s free.

Valmont (VMI) Q3 CY2024 Highlights:

- Revenue: $1.02 billion vs analyst estimates of $1.02 billion (in line)

- EPS: $4.11 vs analyst estimates of $4.00 (2.8% beat)

- EBITDA: $149.8 million vs analyst estimates of $145.7 million (2.8% beat)

- EPS (GAAP) guidance for the full year is $16.90 at the midpoint, roughly in line with what analysts were expecting

- Gross Margin (GAAP): 29.6%, in line with the same quarter last year

- EBITDA Margin: 14.7%, in line with the same quarter last year

- Free Cash Flow Margin: 20.1%, up from 5.3% in the same quarter last year

- Market Capitalization: $6.09 billion

President and Chief Executive Officer Avner M. Applbaum commented, “Our team delivered another solid quarter, expanding operating margins and generating strong operating cash flows despite lower sales. The Infrastructure segment benefited from strong utility market demand and an improving telecommunications market in North America. Pricing discipline, a more favorable product mix, and a leaner cost structure contributed to margin improvement. In Agriculture, while North American and Brazilian markets remain muted, I’m proud of our swift response in supplying replacement equipment to support our dealers following the Midwest U.S. storms earlier this year. I want to thank the Valmont team for their hard work and execution in delivering higher operating margins and cash flows. Overall, I’m pleased with our continued progress towards our strategic priorities and creating long-term value for our stakeholders.”

Company Overview

Credited with an invention in the 1950s that improved crop yields, Valmont (NYSE:VMI) provides engineered products and infrastructure services for the agricultural industry.

Building Materials

Traditionally, building materials companies have built competitive advantages with economies of scale, brand recognition, and strong relationships with builders and contractors. More recently, advances to address labor availability and job site productivity have spurred innovation. Additionally, companies in the space that can produce more energy-efficient materials have opportunities to take share. However, these companies are at the whim of construction volumes, which tend to be cyclical and can be impacted heavily by economic factors such as interest rates. Additionally, the costs of raw materials can be driven by a myriad of worldwide factors and greatly influence the profitability of building materials companies.

Sales Growth

A company’s long-term performance can give signals about its business quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Thankfully, Valmont’s 7.8% annualized revenue growth over the last five years was decent. This shows it was successful in expanding, a useful starting point for our analysis.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. Valmont’s recent history marks a sharp pivot from its five-year trend as its revenue has shown annualized declines of 1.5% over the last two years.

This quarter, Valmont reported a rather uninspiring 2.9% year-on-year revenue decline to $1.02 billion of revenue, in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 3.2% over the next 12 months, an acceleration versus the last two years. While this projection shows the market believes its newer products and services will spur better performance, it is still below the sector average.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) semiconductor stock benefitting from the rise of AI. Click here to access our free report on our favorite semiconductor growth story.

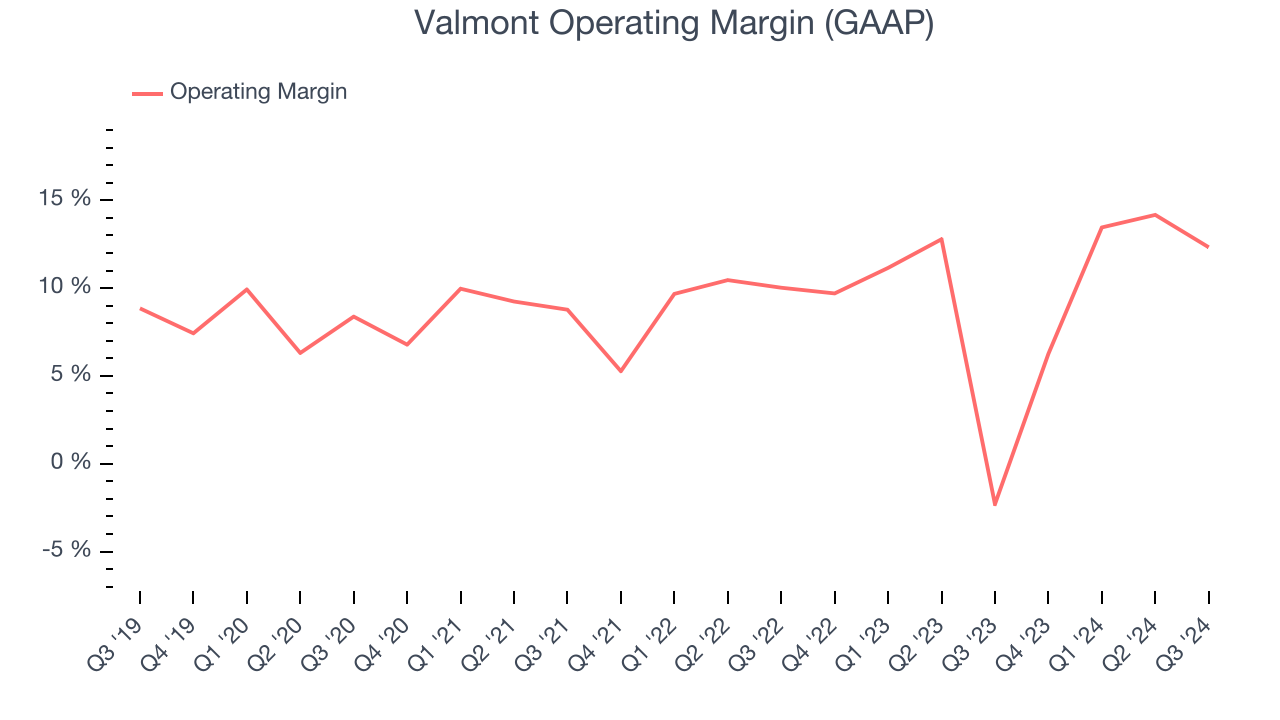

Operating Margin

Analyzing the trend in its profitability, Valmont’s annual operating margin rose by 3.5 percentage points over the last five years, showing its efficiency has improved.

In Q3, Valmont generated an operating profit margin of 12.3%, up 14.6 percentage points year on year. The increase was solid, and since its operating margin rose more than its gross margin, we can infer it was recently more efficient with expenses such as marketing, R&D, and administrative overhead.

Earnings Per Share

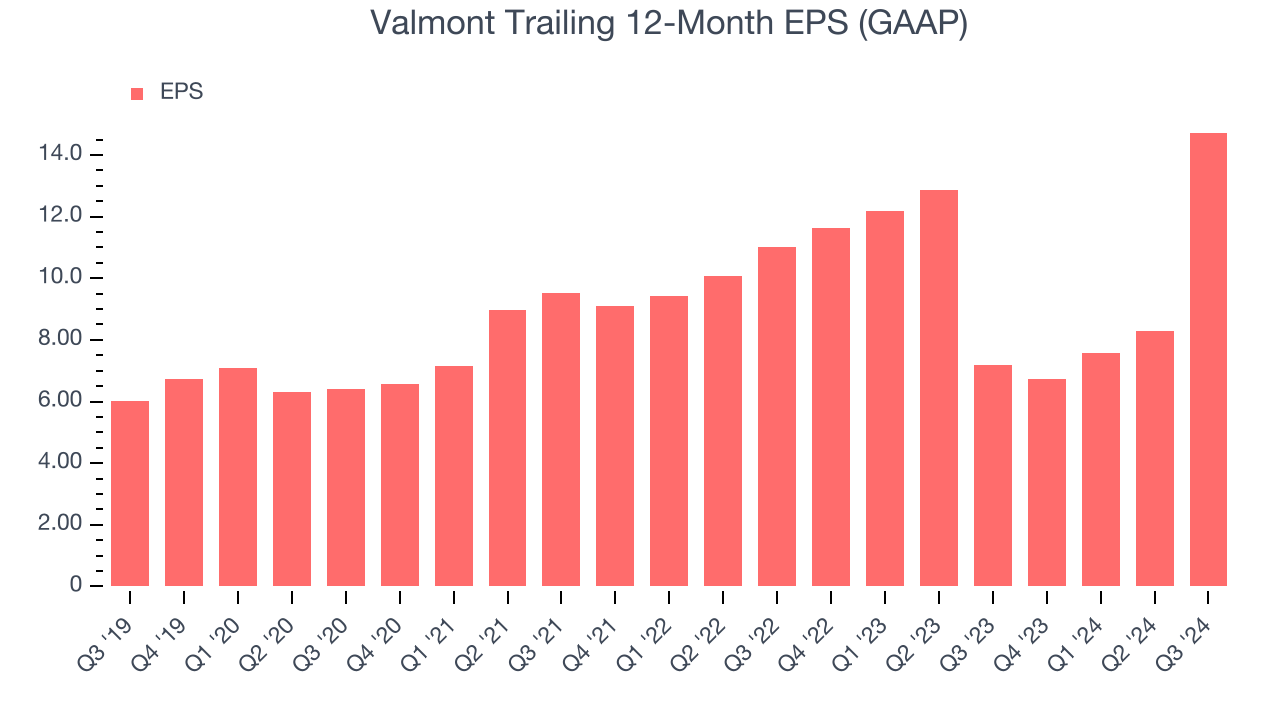

We track the long-term growth in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth was profitable.

Valmont’s EPS grew at an astounding 19.6% compounded annual growth rate over the last five years, higher than its 7.8% annualized revenue growth. This tells us the company became more profitable as it expanded.

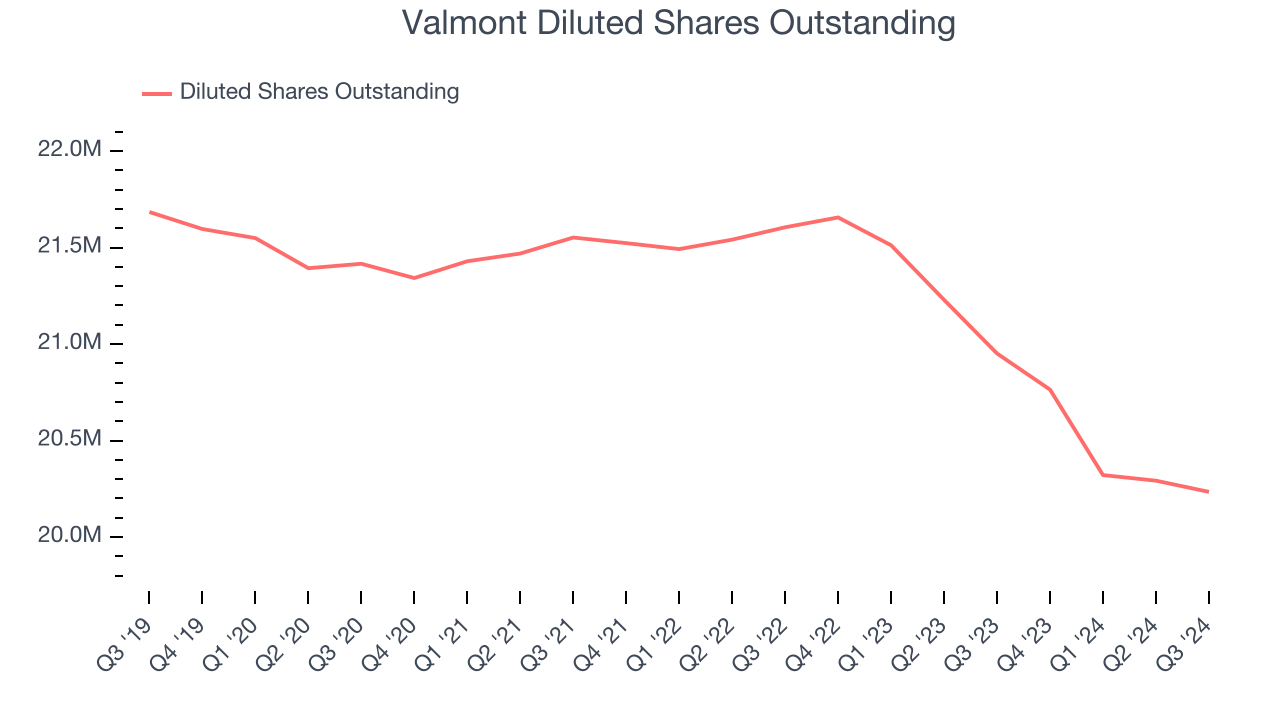

We can take a deeper look into Valmont’s earnings quality to better understand the drivers of its performance. As we mentioned earlier, Valmont’s operating margin expanded by 3.5 percentage points over the last five years. On top of that, its share count shrank by 6.7%. These are positive signs for shareholders because improving profitability and share buybacks turbocharge EPS growth relative to revenue growth.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business. For Valmont, its two-year annual EPS growth of 15.6% was lower than its five-year trend. We still think its growth was good and hope it can accelerate in the future.

In Q3, Valmont reported EPS at $4.11, up from negative $2.34 in the same quarter last year. This print beat analysts’ estimates by 2.8%. Over the next 12 months, Wall Street expects Valmont’s full-year EPS of $14.73 to grow by 22.1%.

Key Takeaways from Valmont’s Q3 Results

It was good to see Valmont beat analysts’ EBITDA expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. Overall, this quarter had some key positives. The stock remained flat at $293 immediately following the results.

Should you buy the stock or not?What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock.We cover that in our actionable full research report which you can read here, it’s free.